Emerging EB Business Insights

Unlock Health Plan Savings With a Balanced Contribution Strategy

SEPTEMBER 2, 2025

In today’s competitive benefits landscape, how employers structure health plan contributions can impact spending more than they might think:

- Contributions can inadvertently incentivize employees to choose the higher-cost plan option.

- Smaller businesses do not have an affordability requirement like larger businesses do. Therefore, employees may seek employment with organizations that are required to offer more affordable coverage (and often richer benefits).

- Larger organizations often contribute to spouse and dependent coverage. Small businesses should review their competitive positioning with respect to dependent contributions.

Employees want options. Having a balance of members on each plan ensures employees get the coverage they prefer, while helping to keep costs low for the company.

Understanding Plan Value

Employers might believe they’re offering a wide diversity of plans based on deductibles, but those plans may be closer in value than they realize. Evaluating plans by “metal tier” is an important part of understanding if employee contributions and out-of-pocket (OOP) expenses are directing members toward the most cost-effective coverage.

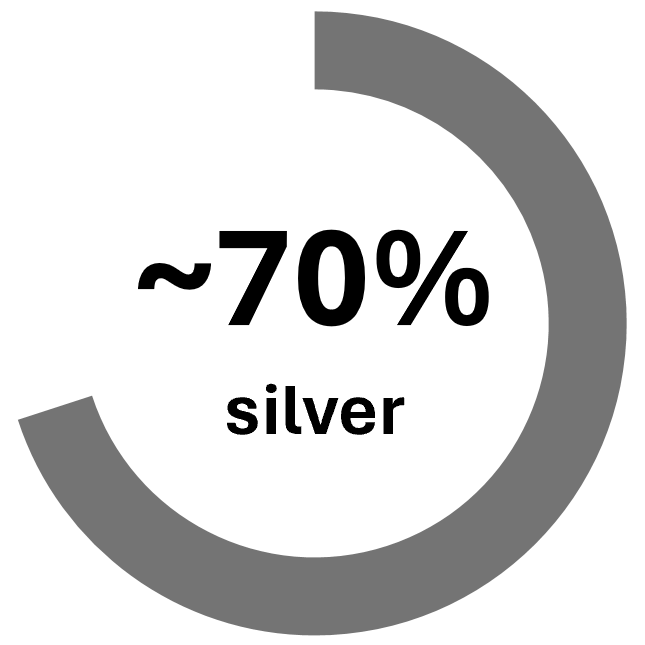

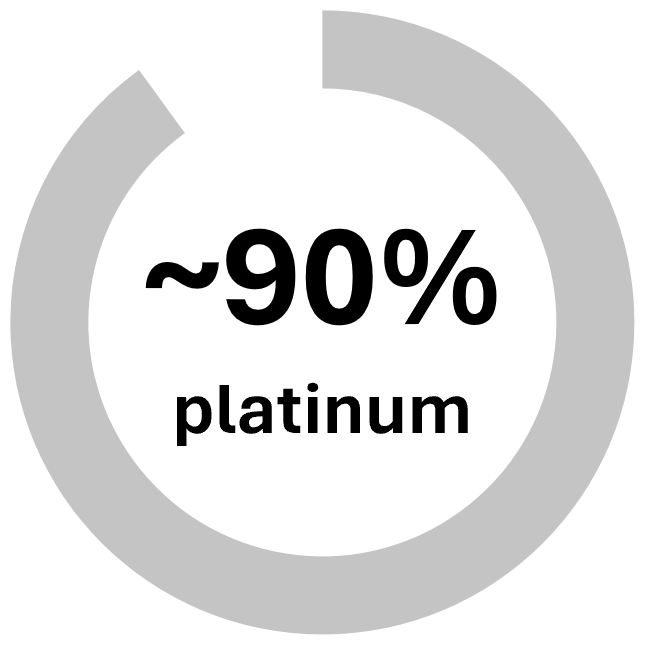

For small businesses, health plans are categorized into levels, aka metal tiers, based on the percentage of medical expense covered by the plan (referred to as “actuarial value,” or AV). As illustrated in the table below, a silver plan covers approximately 70% of medical expenses, while employees cover 30% in the form of out-of-pocket (OOP) costs, like copays and deductibles.

Target Actuarial Value by Metal Tier

|

|

Covers 60% of |

|

|

Covers 70% of |

|

|

Covers 80% of |

|

|

Covers 90% of |

Richer gold/platinum plans offer lower OOP costs for employees, but come with a higher premium. Less rich plans, like bronze and silver, shift more of the cost to employees through higher OOP, but lower the overall cost for employers.

Compare Cost Savings Between Contribution Strategies

Modeling adjustments to a contribution strategy can help employers see the potential cost savings between metal tier options and make changes to ensure benefits are balanced. For example, an employer that currently splits contributions evenly with employees for both a lower-cost silver base plan and higher-cost gold buy-up is incentivizing the majority of plan members into the richer and more expensive plan. Switching to a defined contribution strategy could potentially lower the amount employees pay for the base plan and increase enrollment in the less expensive option.

To ensure plans are competitive with other organizations, contribution modeling should be paired with benchmarking. Benefit plan benchmarking helps employers determine whether their plans are more rich or less rich compared to plans offered by competitor companies, and adjust contributions to better manage health plan spending and employee retention.

How USI Can Help

To help employers understand the value of the health plans they offer, USI Insurance Services uses our proprietary contribution decision support tool to model several predesigned strategies and evaluate the impact of employee migration on overall health plan costs. This can help employers understand what’s driving their employees to specific plans and what changes would provide the most value.

USI can also provide employers with a detailed plan performance assessment, highlighting opportunities to adjust plan design and contribution strategies to make health plans more competitive and affordable. Read our recent article about USI’s Benefits Benchmarking Study to learn how you can request a custom assessment for your company.

Looking at the whole picture — including contribution strategies and OOP expense — can help you align your benefits with employee needs, and better manage health plan spending for your company. Contact your local USI benefits consultant or email ebsolutions@usi.com to learn more.

SUBSCRIBE

Get USI insights delivered to your inbox monthly.