Personal Risk Insights

Protect Your Home and Avoid Costly Insurance Claims

APRIL 1, 2025

From extreme weather to liability claims, homeowners face risks at every turn. Understanding insurance claim statistics can help you make smart investments in preventive measures and reduce the likelihood of suffering a loss.

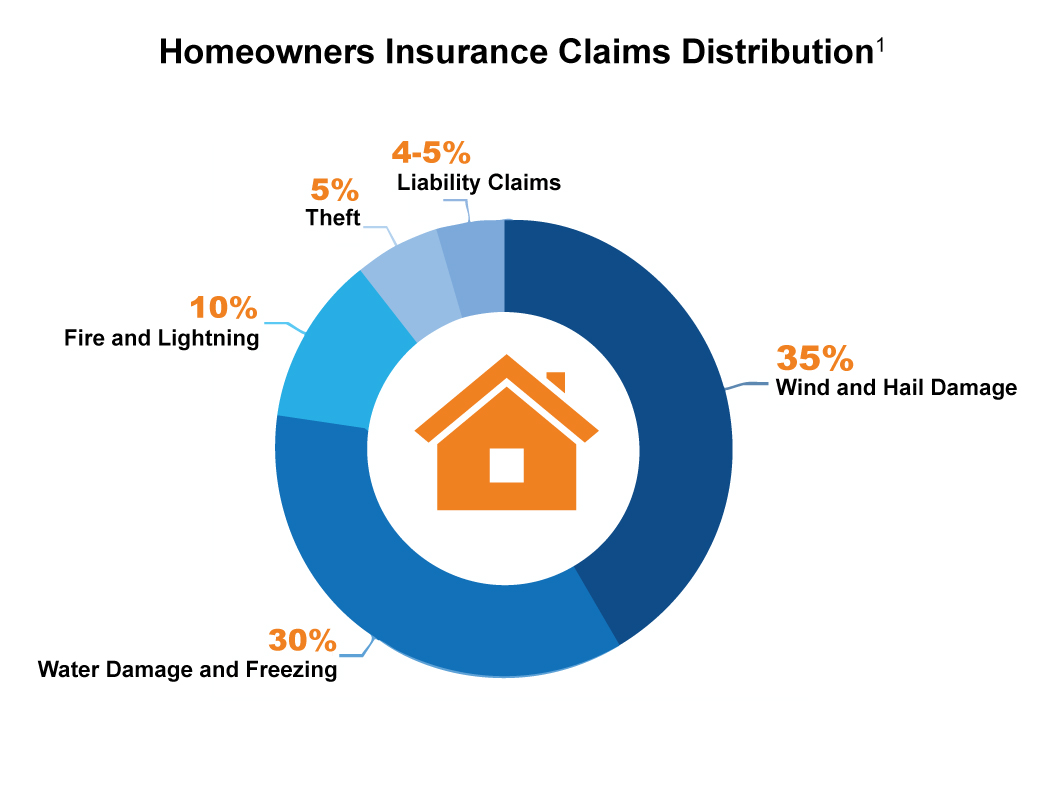

In 2024, the most common homeowners claims in the U.S. were:

To keep your home protected and avoid expensive claims, it helps to know the main causes of loss. Explore the common risks below and practical tips to reduce your exposure.

Wind damage is the most common claim. While Northeast and southern states are at high risk, heavy winds can happen anywhere. To safeguard your home:2,3

- Properly store outdoor items

- Regularly replace loose roof shingles or tiles

- Trim shrubs, trees, and bushes

- Remove branches near the home

- Install window film to keep glass in place if broken

- Regularly inspect your roof to avoid costly repairs

Water-related issues like frozen pipes, plumbing problems, and deteriorating appliance hoses can be costly if not addressed promptly. To prevent and minimize water damage:

Freezing Pipes

- Winterizing your home (insulating pipes, sealing windows and doors, and venting attics to avoid ice dams) can prevent pipe bursts and subsequent water damage

- Remove snow from the roof before it piles up and causes leaks

- Insulate pipes in basements or along exterior walls

Interior Water Damage

- Clean gutters and downspouts

- Check pipes for rust or wear

- Inspect washing machine hoses, including connections

- Check water lines to the fridge

- Inspect water heaters for cracks

- Caulk toilets, sinks, tubs and showers

- Avoid pouring grease down drains

- Install water sensors to detect leaks

- Fix leaks promptly to avoid higher water bills and repair costs

Flood

- Take note of how the land slopes around your property (if it slopes toward your property, water will flow toward your home)

- Install water dams that automatically inflate when wet to stop water from entering your home

- Standard homeowners insurance usually excludes flood coverage, so a separate policy is required

The most expensive home insurance claims are from fire damage. Fires can ignite and spread quickly, which makes damage harder to contain and more severe. Risks include both unavoidable events, such as wildfires, and preventable situations, like forgotten candles, faulty wiring, or carelessness. To minimize losses from a fire:

- Use Class A materials on your roof

- Replace eaves with short overhangs and flat ledges

- Cover exterior attic vents with metal wire mesh (maximum 1/8 inch) to keep embers out

- Create 30 feet of defensible space with noncombustible materials like gravel, brick, or concrete

- Enclose your foundation

- Plan for water access

- Install smoke detectors on each floor and inspect them quarterly

- Keep your home inventory updated

- Get your HVAC and wiring checked

Approximately 51,000 electrical fires happen in the U.S. annually. To prevent them:

- Install an electrical fire safety alert device and service

- Discard frayed, chewed or damaged cords

- Avoid overloading outlets

- Replace loose electrical outlets

- Have your home’s wiring professionally inspected

One in every 325 insured U.S. homes has a property damage claim due to theft each year. Common claims include broken windows or doors. To prevent or reduce losses from theft:

- Lock all doors and windows, including those on your home, garage, garden shed and car

- Avoid leaving your garage door opener in an unlocked car

- Install outdoor motion sensor lights to deter thieves

- Install a centrally monitored security system

- Install cameras, as visible security measures discourage criminals

- Use timers for lights when away to create a lived-in look and deter thieves

If someone slips and falls at your home, you could be liable for their medical bills and legal expenses. This includes uninvited visitors like mail carriers. Avoid these claims by:

- Repairing broken steps or uneven patio stones

- Install hand railings on all stairs

- Removing trip hazards like hoses or loose steps

- Maintain decks and porches by replacing damaged boards and fixing protruding nails

- Promptly remove snow, ice and debris from walkways and driveways

- Secure your pets, even if they don’t bite

- Consider an umbrella policy for extra protection

How USI Can Help

While some events are beyond your control, you can take steps to minimize risk and the likelihood of filing an insurance claim.

USI Insurance Services can help you make informed decisions and maximize asset protection. We create tailored, multipronged, risk management strategies for our clients. To meet with us and discuss your individual insurance needs, contact us at personalriskservice@usi.com.

SUBSCRIBE

Get USI insights delivered to your inbox monthly.